Most people think they understand Bitcoin until they hear some facts about it that sound fake at first.

Most people only know the basics, but once you learn the deeper facts about Bitcoin, it really changes the way you think about it.

Some of these facts might sound a bit crazy at first. But once you understand them, you’ll see why people around the world talk about Bitcoin so much.

What is Bitcoin?

Bitcoin is digital money that only exists online. It runs on a global decentralized network that no bank or government controls. You can use it to send money to people anywhere in the world without a middleman.

Bitcoin became popular worldwide because of its explosive price growth, the massive gains made by early investors, and all the attention it got online and in the media.

However, many people still misunderstand it. Some think it’s mainly used for illegal activities, while others see it as a scam or think it’s too complex. Some people even think it requires a lot of money to start. Because of this, many people miss what Bitcoin really is and how popular it’s become worldwide.

Once you understand the basics, the facts you’re about to learn will make more sense and might even surprise you more.

10 Interesting Facts About Bitcoin Beginners Should Know

Some of these Bitcoin facts will surprise you and make you see Bitcoin differently.

1. A Man Once Spent 10,000 Bitcoin on Two Pizzas

In 2010, a man spent 10,000 bitcoins on two pizzas, a transaction that became one of the most famous stories in Bitcoin history.

Back then, Bitcoin didn’t have a clear market price like it does today, and almost no one saw it as real money. People were mostly trying it out to see if it would work for small payments. That pizza deal was one of the first times Bitcoin was used in real life, and at the time, it felt like a big step forward rather than a mistake.

Fast forward to today, those 10,000 bitcoins would be worth hundreds of millions of dollars. It really shows how much Bitcoin has grown.

The story is now celebrated as Bitcoin Pizza Day, and it’s seen as a symbol of how misunderstood Bitcoin really was.

2. Bitcoin Was Once Worth Less Than One Cent

There was a time when Bitcoin was worth less than a cent, and people could buy thousands of coins for just a few dollars. Back then, hardly anyone knew about Bitcoin, and most people laughed at the idea of money that wasn’t controlled by banks or the government.

Because hardly anyone was using it, very few people thought it would be worth anything in the long run. But as Bitcoin adoption grew worldwide, its value kept going up, turning it from something people once ignored into one of the world’s biggest financial assets.

The story shows that groundbreaking technologies are often underestimated at first, until everyone else comes to understand them.

3. Only 21 Million Bitcoin Will Ever Exist

One of the most important Bitcoin facts beginners should know is that the total Bitcoin supply is permanently capped at 21 million coins. This means there can never be more Bitcoin created, even if Bitcoin becomes very popular later on. Bitcoin’s creator, Satoshi Nakamoto, set this limit to make Bitcoin scarce, similar to gold, which is limited in supply.

This is different from regular money, which governments can print more of whenever they want. Bitcoin is different because its supply stays fixed, no matter how high demand increases. That’s why many people see Bitcoin as a store of value and call it digital gold.

As more investors, companies, and even countries adopt Bitcoin, people believe its limited supply will make even a small amount more valuable in the future.

Understanding Bitcoin’s fixed supply is one reason many beginners want to learn how to invest in it. If you’re not sure how people invest safely, here’s a guide to help.

4. Around 20% of All Bitcoin Are Permanently Lost Forever

Not stolen. Not hidden. Just gone. Some researchers believe that about 20% of all bitcoins may be lost forever. Many owners forgot their passwords, lost their recovery phrases, or passed away without giving anyone access to their wallets.

When Bitcoin first came out, a lot of users didn’t take it seriously because they didn’t think it would ever be worth anything. The surprising part is that those coins are still on the blockchain, but they can’t be moved or spent anymore.

Stories like these are why people take secure crypto storage and backup recovery phrases so seriously now.

Lost bitcoins reduce the total amount of Bitcoin in circulation, so it gets even scarcer.

Bitcoin introduced a new form of wealth where people have full ownership, but also have to protect it themselves.

5. Some Bitcoin Wallets Have Been Silent for Over 14 Years

One of the most fascinating Bitcoin facts is that some wallets haven’t had any activity in over 14 years. Many of them contain massive amounts of Bitcoin from the early days of Bitcoin, when mining was easy and Bitcoin was barely worth anything.

Some are from owners who’ve held onto their coins for a long time and never moved them. Others are from people who may have forgotten they even had them.

What makes this different from Bitcoin that’s considered permanently lost is the uncertainty about whether those wallets can still be opened. So when an old wallet suddenly becomes active, it tends to get a lot of attention.

Crypto traders track blockchain activity closely because a big transfer can get everyone talking. People start wondering if the owner recovered their wallet access, returned after years away, or if it’s someone linked to Bitcoin’s creation.

6. Nobody Truly Knows Who Created Bitcoin

Nobody really knows who created Bitcoin. It was introduced to the world under the name Satoshi Nakamoto, but the real identity is still unknown.

In the early days, Satoshi worked closely with other developers online, communicating a lot and helping shape the system as it came together. Over time, he started communicating less, stepped back, and eventually disappeared from public view.

Since then, people have come up with many theories about Satoshi’s identity, but none of them have been proven yet.

Bitcoin is unique because no one knows who created it, and no single person or organization controls it. Some people also believe that the early Bitcoin wallets linked to Satoshi Nakamoto haven’t been accessed since the early days.

7. Every Bitcoin Transaction Can Be Traced

Every Bitcoin transaction is traceable because the Bitcoin blockchain keeps a public record of all transactions.

One of the biggest misconceptions about Bitcoin is that it’s completely anonymous. In reality, it’s pseudonymous. Wallet addresses are visible to everyone, but usually, people don’t know who they belong to.

This transparency lets anyone independently verify Bitcoin transactions, so analysts, companies, researchers, and law enforcement can all track where money is going. It also lets analysts keep an eye on network activity, including large Bitcoin wallets, often called whales, and monitor big Bitcoin transfers as they happen.

8. Bitcoin Transactions Cannot Be Reversed

Imagine you accidentally send money to the wrong address and realize there’s no one you can call to reverse it. That’s how Bitcoin works.

Once a Bitcoin transaction is confirmed, it’s final and can’t be reversed. That’s by design because no bank, company, or central authority controls it.

While traditional payment systems usually allow refunds, disputes, or chargebacks, Bitcoin works a bit differently. So there are both upsides and downsides. You’re more in control of your money, and there’s less risk of fraud, but if you make a mistake, it’s basically impossible to fix.

That’s why experienced crypto users double-check wallet addresses and transaction details before sending money.

What makes this fact important is that Bitcoin shifts responsibility away from institutions and puts it in your hands.

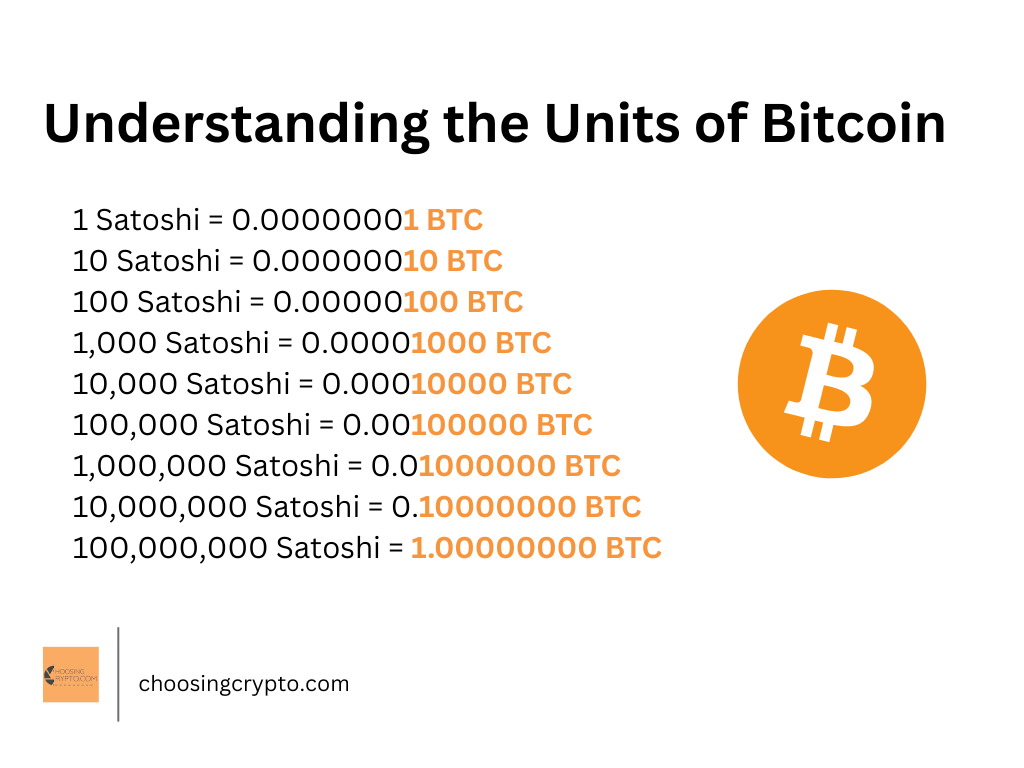

9. You Don’t Need to Buy a Whole Bitcoin

Many people think you need to buy a whole Bitcoin before you can invest. But that’s not true. You can buy as little or as much Bitcoin as you like. That’s because Bitcoin is divisible into 100 million smaller units called satoshis.

1 BTC=100,000,000 satoshis.

Because of this, owning Bitcoin is more accessible than most people think. Even a small purchase gives you a fraction of a Bitcoin, so beginners can get started easily.

As a result, many crypto exchanges now let you start with a small amount of money. For example, platforms like Bybit and Gate.io let you buy fractions of a Bitcoin with just $10.

10. Bitcoin Mining Uses More Electricity Than Some Countries

One of the most surprising facts about Bitcoin is that mining it can use more electricity than some countries. This happens because miners around the world use powerful computers to solve complex math problems that verify transactions and keep the Bitcoin network secure.

The massive computing power used in this process, called Proof-of-Work, helps protect against fraud and attacks, and that’s what makes Bitcoin one of the most secure digital networks.

While critics argue that the energy consumption is harmful to the environment, supporters believe it’s worth it to maintain a decentralized financial system.

As Bitcoin adoption grows, its energy use is still one of the most debated topics about it.

Why These Bitcoin Facts Matter

When you put all these Bitcoin facts together, you start to see the bigger picture. Bitcoin isn’t just about price changes. It’s about scarcity, transparency, decentralization, security, and the way people react to new technology.

Many people ignored it at first because they didn’t really understand it. This shows how often we overlook important innovations at the beginning. The real lesson is not regret, but understanding what people missed.

Instead of chasing hype, it’s better to learn how Bitcoin works and how it’s different from regular money.

For beginners, understanding Bitcoin is usually more important than owning it. The more you understand how it works, the better your decisions will be when you invest.

If you’re interested in Bitcoin but still not sure how to buy it safely or avoid scams, I can help. I teach beginners the basics and show you how to avoid common mistakes. Learn more here.

Conclusion

Learning these Bitcoin facts is a good start, but it’s even better if you really understand Bitcoin instead of just knowing a few interesting things about it.

The next step is learning how Bitcoin works, the safest ways to buy it, and how to keep it safe once you have it.

Start with the guides below:

- What is Bitcoin and How Does it Work?

- How to Buy Cryptocurrencies like Bitcoin Safely (Even as a Beginner)

- 7 Common Crypto Mistakes Investors and Traders Make

FAQs

And guess what? We’re also on Instagram and Twitter(X). Join us there for even more fun and useful content!

DISCLAIMER:

The information provided here is intended for informational purposes only and should not be solely relied upon for making investment decisions. It does not constitute financial, tax, legal, or accounting advice. Additionally, I strongly recommend only investing money in cryptocurrency that you are comfortable losing.